Dividend-Paying Small-Cap Stocks and Investment Performance

March 20, 2026

Dividend policy has long been a subject of debate in financial economics. Classical theory suggests that dividend policy should not affect firm value, yet empirical research frequently identifies systematic differences in the performance of dividend-paying and non-dividend-paying firms. Here, we review some of the available academic literature on dividend-paying equities with particular emphasis on small-capitalization stocks.

Summary

Evidence from peer-reviewed studies and research published by the CFA Institute indicates that portfolios composed of dividend-paying firms have historically generated higher average returns and lower volatility than portfolios composed solely of non-dividend-paying stocks.

However, modern asset-pricing research suggests that much of the observed dividend premium can be explained by exposure to risk factors associated with value, profitability, and investment patterns rather than by dividend payments themselves.

The literature therefore suggests that dividend strategies function primarily as screening mechanisms that identify financially robust firms rather than as independent sources of excess return.

Introduction

Dividend policy has been one of the most extensively studied topics in corporate finance and asset pricing. The debate gained prominence with the work of Franco Modigliani and Merton H. Miller, whose influential study Dividend Policy, Growth, and the Valuation of Shares established the dividend irrelevance proposition. Their theoretical model demonstrates that under conditions of perfect capital markets, a firm's dividend policy should not affect its valuation.

Despite this theoretical conclusion, numerous empirical studies have documented persistent differences in the performance of dividend-paying and non-dividend-paying firms. Dividend-paying companies often exhibit characteristics such as stronger profitability, lower volatility, and more stable earnings streams. These characteristics may influence investor expectations regarding risk and expected returns.

The relationship between dividend policy and performance may be particularly relevant for small-capitalization firms. Smaller firms generally face greater information asymmetry, higher earnings volatility, and more limited access to external financing than large corporations. As a result, dividend payments by small firms may serve as signals of financial strength and operational maturity.

This paper reviews the academic literature on dividend-paying stocks with a particular emphasis on the small-cap segment of the equity market, synthesizing theoretical explanations and empirical findings from peer-reviewed research and CFA Institute publications.

THEORETICAL PERSPECTIVES ON DIVIDEND POLICY

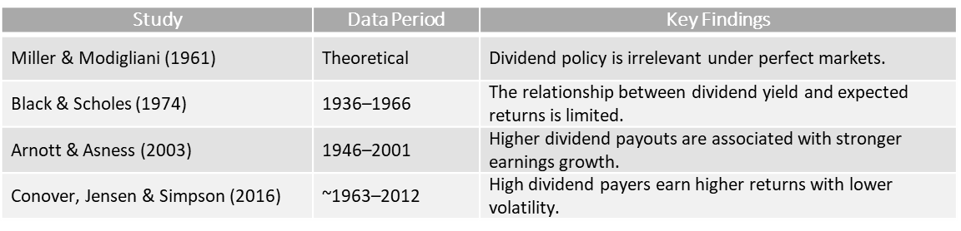

Dividend Irrelevance. The dividend irrelevance proposition developed by Miller and Modigliani (1961) states that dividend policy should not influence firm value in a frictionless market environment. Under their model, investors can replicate dividend income through “homemade dividends” (i.e., investors can create their own cash flow by selling shares), rendering corporate dividend policies irrelevant.

Although the model provides an important theoretical benchmark, it relies on assumptions that rarely hold in practice. Real-world capital markets are characterized by taxes, transaction costs, and information asymmetries, all of which may create conditions in which dividend policy becomes relevant.

Agency Theory and Free Cash Flow. Agency theory provides an alternative explanation for the potential relevance of dividends. Michael C. Jensen proposed the free cash flow hypothesis in Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers, arguing that managers may invest excess corporate cash in projects that do not maximize shareholder value.

Dividend payments reduce the amount of discretionary cash available to managers, thereby limiting the potential for inefficient investment decisions. In this sense, dividend distributions may reduce agency costs and improve corporate governance.

Dividend Signaling. Another explanation for dividend policy is the signaling hypothesis. Because managers typically possess more information about future earnings prospects than outside investors, dividend changes may convey information about expected firm performance.

Managers are often reluctant to reduce dividends once they have been established, making dividend increases a credible signal of confidence in future earnings. This signaling mechanism may be especially important among small firms where information asymmetry is greater.

EMPIRICAL EVIDENCE ON DIVIDEND-PAYING STOCKS

Early Empirical Studies. Early empirical work by Fischer Black and Myron Scholes in The Effects of Dividend Yield and Dividend Policy on Common Stock Prices and Returns examined whether dividend yields influenced stock returns after controlling for risk.

Their results suggested that dividend policy had limited explanatory power for expected returns once risk factors were accounted for. However, later research identified more complex relationships between dividend policy and stock performance.

Evidence from Long-Term Market Data. A comprehensive empirical study by C. Mitchell Conover, Gerald R. Jensen, and Marc W. Simpson in What Difference Do Dividends Make? analyzes more than five decades of U.S. equity market data.

The authors find that high-dividend-paying stocks exhibit lower volatility and higher average returns than non-dividend-paying stocks. Their results indicate that portfolios composed of high-dividend-paying firms outperform portfolios of non-dividend-paying firms by approximately 1.5 percentage points annually, while also displaying lower risk.

Importantly, the study also finds that the benefits of dividend exposure vary across market segments.

Dividend Exposure in Small-Cap Portfolios. Research summarized by the CFA Institute indicates that dividend exposure has particularly strong effects within small-cap portfolios.

Using long-term U.S. equity data, the analysis finds that increasing dividend exposure significantly improves portfolio performance. In small-cap portfolios, increasing dividend exposure from none to high increases returns by approximately 26 basis points per month.

The improvement is especially pronounced among small-cap growth stocks, which traditionally are assumed to benefit from reinvesting earnings rather than distributing dividends. These findings suggest that dividend payments may help identify financially strong firms within the small-cap universe.

DIVIDEND YIELD AND RETURN PREDICTABILITY

Another strand of research examines whether dividend-related variables help predict future stock returns. Robert D. Arnott and Clifford S. Asness demonstrate in “Surprise! Higher Dividends = Higher Earnings Growth” that higher dividend payout ratios are associated with stronger future earnings growth. These findings challenge the traditional view that high dividend payouts necessarily constrain corporate growth.

ALTERNATIVE EXPLANATIONS: FACTOR EXPOSURE

Although empirical studies frequently find superior performance among dividend-paying firms, many researchers argue that this effect can be explained by exposure to well-known risk factors.

The Fama–French three-factor model, developed by Eugene F. Fama and Kenneth R. French, identifies firm size and value characteristics as important determinants of stock returns. Dividend-paying firms frequently exhibit higher book-to-market ratios and more stable profitability, characteristics associated with the value factor.

Later work by the same authors in the A Five-Factor Asset Pricing Model introduced profitability and investment factors, both of which are commonly observed among dividend-paying companies. These results suggest that the performance advantage of dividend-paying stocks may largely reflect exposure to these underlying factors.

SUMMARY OF MAJOR DIVIDEND STUDIES

Selected Academic Studies on Dividend Policy and Stock Returns

SMALL-CAP DIVIDEND PERFORMANCE

Empirical studies examining portfolio construction show that dividend-paying firms in the small-cap segment often demonstrate:

Higher profitability

Lower volatility

Lower financial distress risk

These characteristics may explain why dividend-paying small-cap stocks tend to exhibit superior risk-adjusted returns.

LIMITATIONS OF DIVIDEND-BASED STRATEGIES

Despite the historical performance advantages observed in many studies, dividend-focused strategies have several limitations:

Reduced investment universe: Many high-growth firms do not pay dividends.

Sector concentration: Dividend-paying firms are often concentrated in certain industries.

Changing market conditions: Return patterns identified in historical data may weaken as investors incorporate them into trading strategies.

OUR PERSPECTIVE

The academic literature provides substantial evidence that dividend-paying stocks have historically exhibited different performance characteristics than non-dividend-paying firms. In particular, research suggests that dividend-paying small-cap stocks often generate higher returns and lower volatility.

However, modern asset-pricing models indicate that much of the observed dividend premium may be explained by underlying firm characteristics such as valuation, profitability, and investment behavior rather than dividend payments themselves.

Consequently, dividend-focused investment strategies may function primarily as screening mechanisms that identify financially stable firms with favorable factor exposures, rather than as independent drivers of excess returns.

Contact Jay Young (jay.young@vergencepartners.com) or me (tom.douglas@vergencepartners.com) with any comments or questions. Visit www.vergencepartners.com and follow us on LinkedIn to see what else we’re thinking about.

References

Arnott, R. D., & Asness, C. S. (2003). Surprise! Higher dividends = higher earnings growth. Financial Analysts Journal.

Black, F., & Scholes, M. (1974). The effects of dividend yield and dividend policy on common stock prices and returns. Journal of Financial Economics.

Conover, C. M., Jensen, G. R., & Simpson, M. W. (2016). What difference do dividends make? Financial Analysts Journal.

Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics.

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review.

Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. Journal of Business.

FOR INSTITUTIONAL USE ONLY

Vergence Institutional Partners LLC is registered as an investment adviser with the states of KY, MA, MI, RI, and TN. Vergence Institutional Partners LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

This report is a publication of Vergence Institutional Partners LLC. It is intended only for use by plan sponsors and fiduciaries. Information presented is believed to be factual and up to date, but we do not guarantee its accuracy, and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change.

Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

Vergence Institutional Partners LLC does not provide advisory services to individuals.

Vergence Institutional Partners LLC does not provide legal or tax advice. Please consult your tax or legal advisor to address your specific circumstances.

Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client's investment portfolio.

Historical performance results for investment indexes or categories generally do not reflect the deduction of transaction and custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. You cannot invest directly in an index.

Economic factors, market conditions, and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

20260401TLDTLD0058

© 2026 Vergence Institutional Partners LLC